Total Views: 6643

Total Views: 6643

Table of Content

Blog Summary:

This blog post is targeted towards entrepreneurs, businesses, and individuals interested in the fintech industry and developing their neobank app. It provides a comprehensive overview of Neobank App Development, business models, development process, and market potential. Overall, it’s a useful guide for anyone considering a venture in this space.

Table of Content

The world has shifted online, and so have we. From ordering food to getting a medical consultation, digital solutions have become the new normal. And banks are no exception.

Mobile banking is extremely popular in the United States, with over 76% of customers utilizing banking apps.

We’ve all grown accustomed to mobile banking apps and websites, but today’s younger generation can handle almost any financial task without ever setting foot in a physical branch. The trend is clear: digitalization is the future. So, the question isn’t whether to adapt, but how. The answer? Create your own neobank.

In this article, you’ll learn everything about building a neobank from scratch. We are identifying the essential steps and business requirements that address the critical cost considerations as well.

Neobanks are financial technology (fintech) companies that offer banking services exclusively through digital channels. These organizations do not have any physical branches. It is primarily a significant part of the “fintech” movement. The main objective of a neobank is to provide a more modern, convenient, and affordable banking experience.

Users primarily interact with a neobank through a dedicated mobile app. These apps are intuitive and user-friendly, accessible anywhere and at any time, provided an internet connection is available.

Another defining characteristic of neobanks is that they incur no overhead costs associated with maintaining brick-and-mortar locations. As a result, neobank apps offer either lower fees or better interest rates to customers.

Moreover, neobank apps are designed to provide a seamless and efficient user journey. This includes features such as quick account opening, real-time notifications, and simplified financial management tools.

The development of these apps leverages modern technologies, including AI, ML, and cloud computing. Consequently, neobank applications offer advanced features, personalized insights, and robust fintech security.

If you are looking for different models of the neobank apps, here’s the breakdown. Let’s check them out in detail:

In this model, neobanks provide financial products and services directly to individual consumers. Their primary appeal lies in offering a digital-first experience through easy onboarding, an intuitive user interface, and 24/7 access to banking services.

Moreover, neobanks offer competitive or even fee-free accounts because they operate without a physical bank. Users receive personalized financial insights and innovative features, as the neobank app leverages useful customer data and AI, which traditional banks often lack.

Additionally, some B2C neobanks focus on particular demographics, such as millennials, gig economy workers, and immigrants. They can also be niche-based, catering to specific needs, including travel-focused banking and green banking.

Examples of B2C models include Chime (US), Revolut (UK), N26 (Germany), and Monzo (UK).

In this model, the fintech organizations don’t directly offer banking services to end-users. Instead, they provide the underlying technological infrastructure and regulatory banking license that other businesses can “plug into” to offer their financial products. Essentially, they act as a backend provider for banking functionalities.

One key characteristic of the B2B BaaS model is that it enables non-financial businesses to integrate financial services directly into their products or services. This is also referred to as “embedded finance”.

Many third-party providers partner with traditional banks to provide online banking services, as they may not hold a full banking license themselves. This allows them to offer a wide range of services to customers while the partner bank handles the regulatory compliance and risk.

The B2B BaaS services are also provided through application programming interfaces (APIs). It allows seamless integration of banking functionalities into existing business systems. Examples of BaaS models include Solarisbank (Germany), Railsbank (UK), and Synapse (US).

Neobanks utilize a diverse range of revenue streams to achieve profitability. It combines several sources from the following:

The first one is interchange fees, which are a foundational revenue source, especially for those neobanks issuing debit or credit cards. It works like this – when a customer uses their neobank-issued card to make a purchase, the merchant’s bank pays a small percentage of the transaction value (the interchange fee) to the issuing bank (which is the neobank or its partner bank).

The next one is lending (Net Interest Income). Neobanks that hold a banking license or partner with licensed banks to offer lending products become a major profit driver. This works as follows – they earn money from the interest charged on loans, credit cards, overdrafts, and Buy Now, Pay Later (BNPL) services.

This is a more capital-intensive but potentially higher-margin revenue stream compared to interchange fees.

The third one is subscription fees/premium accounts. Many neobanks adopt a “freemium” model. Here’s how it works – they offer a basic account for free to attract a large user base. Thereafter, it provides premium tiers with enhanced features for a recurring monthly/annual subscription fee.

The next model is value-added services & transaction fees. Neobanks often charge fees for specific services beyond basic account operations. These include foreign exchange (FX) mark-ups, out-of-network ATM fees, expedited payments or transfer funds, and commissions for cryptocurrency trading.

The fourth revenue source of neobanks is through marketplace banking and referrals. Some neobanks offer a marketplace within their mobile app where users can access curated products.

These may include mortgages, insurance, pensions, or other financial services provided by partner companies. Here, the neobank earns a referral fee/commission for facilitating these connections.

Last but not least – “float income”. This is less relevant than other revenue streams, but neobanks earn interest on the deposits held by their customers, particularly on idle balances. This is the interest earned by the bank from investing customer deposits before they are withdrawn.

Neobank apps provide a mobile-centric experience, often with lower fees and personalized services. Let’s head to its working structure:

Neobank apps are developed using modern, cloud-native, and microservices-based architectures. This enables scalability, agility, and the real-time processing of transactions. Moreover, they use APIs to connect various services and often incorporate AI and machine learning for personalization and fraud detection.

It is an entirely online process that allows users to open accounts quickly. This involves collecting personal information, often using automated tools for know your customer (KYC) verification.

It’s an essential part of onboarding to verify a customer’s identity. It involves submitting a government-issued ID, typically with biometric verification. The automated tools compare submitted data against databases to ensure accuracy and prevent fraud. Ongoing monitoring of financial transactions is also a key component of AML (Anti-Money Laundering) compliance.

The virtual cards are digital payment instruments generated and hosted online. They operate like physical cards, featuring a 16-digit number, a CVV, and an expiry date.

Virtual cards are convenient to use as they are easily managed within the neobank app. These cards also provide enhanced security as they often come with spending limits that reduce the risk of fraud.

Neobank apps are designed for instant processing, enabling payments, transfers, and account updates to occur in real-time. Hence, these apps provide users with immediate visibility into their finances.

APIs (Application Programming Interfaces) are fundamental for software development. They enable neobanks to seamlessly integrate with third-party payment providers, fintech apps (e.g., budgeting tools, investment platforms), and regulatory platforms, thereby expanding their service offerings and creating a broader financial ecosystem.

Neobank apps are heavily regulated, apart from their entirely digital nature. They implement robust compliance programs, including anti-money laundering and CFT (Combating the Financing of Terrorism) measures. This involves rigorous KYC, continuous transaction history monitoring, and adherence to general data protection regulations.

Moon Technolabs has years of experience in crafting high-performance neobank apps that meet compliance, security, and scalability standards.

There are numerous reasons to build a neobank app in 2025. It presents a significant opportunity, complemented by favorable market trends and growth projections. Additionally, it provides distinct competitive benefits and a clear demand from the intended users.

Many neobanks have achieved remarkable success by extending banking services to previously underserved populations or by providing existing customers with the benefits of lower fees and integrated features.

The neobank market is rapidly expanding, and future saturation is unavoidable. This means that without a well-thought-out strategy, promoting your neobank app will become increasingly challenging.

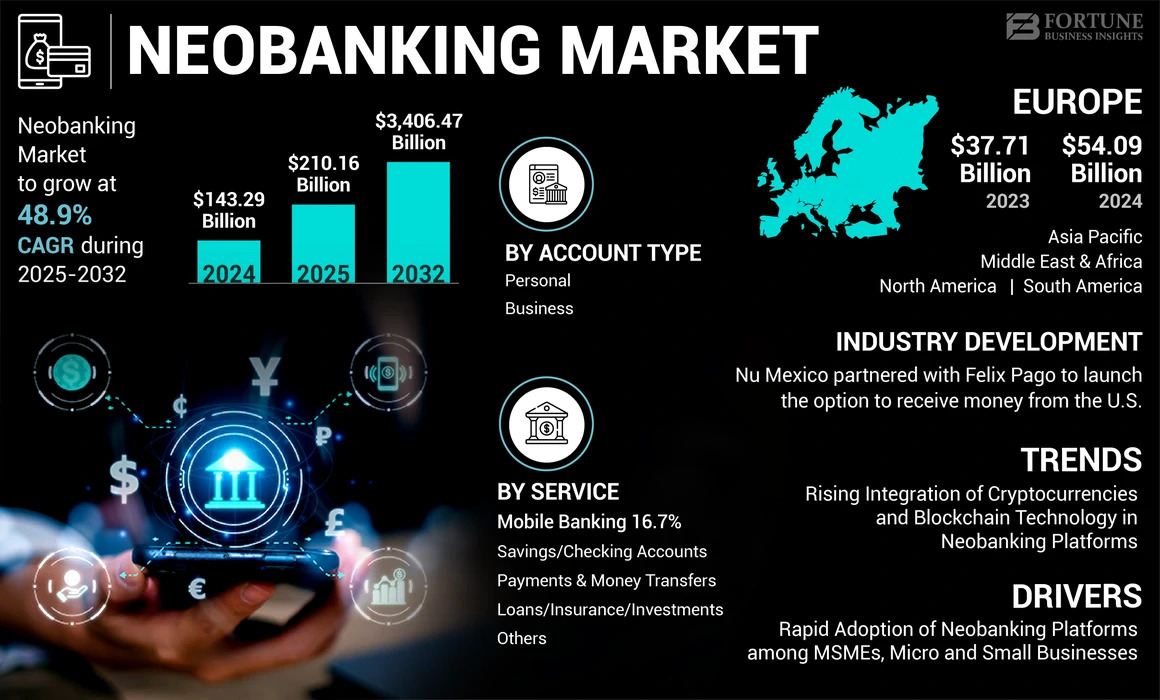

Now, let’s understand the neobank market size & forecast according to Fortune Business Insights. Refer to the short table below:

| Metric | Value |

|---|---|

| 2024 Market Size | $143.29 billion |

| 2032 Market Size Projection | $3,406.47 billion |

| CAGR (2024-2032) | 48.9% |

| Largest Market (2024) | Europe (37.75% share) |

These figures highlight the growing demand for neobanks. Hence, now is the critical time to start your robust fintech (neobank) app development. So, act decisively, establish a strong presence, gain a crucial first-mover advantage, and capitalize on the favorable market conditions before the landscape becomes more competitive.

Are you still skeptical about the future of neobanking? Let’s explore the compelling advantages of developing a neobank app.

The benefits are evident across various aspects of the financial industry, driven by a digital-first approach and the innovative use of technology:

Since there are no physical units, the overhead charges of a neobank app are significantly lower than those of traditional banking services. App users can also take advantage of this benefit in the form of incredible offers, along with no-cost services.

Neobanks outdo geographical limitations, making financial services available to anyone with a smartphone, anywhere in the world. They effectively bridge the gap for the underbanked and unbanked populations, who often face barriers with traditional institutions.

This digital-first approach enables rapid market expansion, providing easy access to diverse demographics and emerging economies. Moreover, it is a convenient approach, as 24/7 mobile access attracts users who prefer to manage their finances on their terms.

Neobank apps prioritize intuitive interfaces and seamless navigation, making banking a seamless experience. It delights users through features like lightning-fast onboarding and personalized financial dashboards.

Real-time notifications, intelligent budgeting tools, and integrated P2P payments create a highly interactive and valuable financial journey. The app’s focus on user-centric design transforms complex financial tasks into simple, engaging actions.

Real-time analytics is a powerful tool for dynamic fraud detection and optimizing services. It moves banking from reactive statements to proactive, data-driven financial management for both customers and the bank.

Neobanks lower barriers, such as fees and minimum balances, offer alternative credit scoring, and reach underserved areas, making financial services more accessible to a broader range of people.

You can develop a robust neobank app with unique features and functionalities. Check them out below:

It is one of the most important features of developing a neobank app. Digital onboarding is not just about filling out online forms. The neobank app offers a truly paperless and instant account opening process, which takes just a few minutes to complete.

Here, optical character recognition (OCR) technology is used for swift document scanning. Robust video know your customer (KYC) for real-time identity verification. It ensures regulatory compliance and provides a frictionless user experience from any location.

This feature does not just allow balance and transaction checking. It is a comprehensive control center for the user’s finances. Additionally, it offers seamless management of virtual and physical cards.

Users can set limits, freeze or unfreeze transactions, reorder cards, and view detailed spending analytics. Not only that, they can initiate various types of fund transfers (IMPS, NEFT, RTGS), and set up recurring payments or standing instructions, all within a clean and intuitive interface.

This feature transforms raw transaction data into actionable financial intelligence. By utilizing ML algorithms, the app automatically categorizes expenses and identifies spending patterns. It also provides personalized recommendations for saving, budgeting, and investing.

For instance, highlighting areas of overspending, suggesting ways to optimize recurring bills, and even nudging users towards savings goals, making financial management proactive and insightful.

Given the digital-first nature, robust security is paramount. Neobanks in India utilize multi-layered authentication. This includes biometric login methods, such as fingerprint or facial recognition, as well as two-factor authentication (2FA).

This feature ensures that users are always aware of their financial activities as they occur. Instant push notifications for every transaction (debit/credit), low balance alerts, bill payment reminders, and even suspicious activity alerts provide immediate awareness and control.

This proactive communication enables users to closely monitor their funds and respond swiftly to any anomalies, thereby enhancing security and promoting financial peace of mind.

This is a crucial offering for digital-first users. Neobanks provide instantly issued virtual cards that can be used for online purchases, UPI payments and digital wallet integrations even before a physical card arrives.

Users can easily manage these virtual cards within the app, including setting daily limits, temporarily blocking them for security, or generating single-use card numbers for enhanced protection against online fraud.

Recognizing the absence of physical branches, accessible in-app support is vital. Neobank apps integrate AI-powered chatbots that can answer frequently asked questions, guide users through common processes, and even troubleshoot basic issues around the clock.

For more complex queries, seamless escalation to human customer support is available directly within the app, providing convenient and efficient assistance via chat or call.

In the Indian context, deep integration with the Unified Payments Interface (UPI) is non-negotiable, enabling instant and seamless peer-to-peer and merchant payments directly from the app. Beyond UPI, robust integration with major card networks (Visa, Mastercard, RuPay) ensures global acceptance.

Furthermore, linking with popular digital wallets like Google Pay and Apple Pay enhances payment flexibility and convenience for users, making the neobank app a central hub for all financial transactions.

Our experts at Moon Technolabs are ready to take charge and build your project with precision and power. Right from strategizing to launching your app, we’ve got you covered.

Neobank app development is a complex undertaking that requires a deep understanding of financial regulations, technology, and user experience. Below, we outline a comprehensive, step-by-step process:

The first and foremost step is thorough market research and meticulous compliance planning.

So you need to identify your niche. Neobanks have a higher chance of success if they are well-targeted to specific demographics or underserved markets, such as freelancers, small businesses, or specific age groups. Understand their unique financial needs, pain points, and preferences.

Thereafter, you need to analyze both existing neobanks and traditional banks. For that, figure out: what are their strengths and weaknesses? What features do they offer? How do they acquire and retain customers? Identify gaps you can fill.

Moreover, assess the market size, potential revenue streams, and the overall viability of your proposed neobank. Lastly, develop a user persona that includes details such as their financial habits, technological proficiency, and motivations.

Research local financial regulations like AML, KYC, data privacy (GDPR/CCPA), and consumer protection laws.

There are many licensing options, like a full banking license, an EMI license, and a bank partnership. Set up strong internal compliance policies, including fraud prevention, risk management, and staff training.

The user interface and user experience are critical for neobank mobile app development, as they directly impact user adoption. Here are a few tips for that:

This is the most crucial step in the neobank development process. You have two primary options: build or buy. Building a core banking system is highly complex & costly. For neobanks, the most common approach is to integrate the app with a third-party core banking system.

Partner with a Banking-as-a-Service (BaaS) provider. For example, Galileo, Unit, Synapse, Mambu, and Temenos offer modular APIs for various banking functionalities. This is the most common approach for neobanks.

Services Offered by BaaS:

Benefits of BaaS:

Moreover, evaluate different providers based on their API capabilities, scalability, security, regulatory compliance, pricing models, and track records.

The backend is the engine that powers your neobank app. It handles data, logic, and integrations. First, choose a robust and scalable technology stack:

Then comes the API Development part. The following parts are the most important among them.

This is a non-negotiable phase. It involves comprehensive testing of every aspect of the app, including functional testing, performance testing, usability testing, and, most critically, rigorous security testing (e.g., penetration testing, vulnerability assessments) to identify and rectify any potential flaws. It is important to protect user information and maintain trust by ensuring top-tier security and bug-free operation.

Once the app has passed all tests and received necessary regulatory approvals, it is deployed to app stores. However, the work doesn’t stop there. Continuous monitoring, bug fixes, regular updates, feature enhancements based on user feedback, and dedicated customer support are essential for the long-term success, growth, and sustained user satisfaction of your neobank.

The cost of developing a neobank app depends on several factors, including the app’s complexity, design requirements, and the choice of platform (iOS, Android, or both).

It also depends on third-party integrations such as KYC and payment gateways, security protocols, and the location & expertise of the development team. Let’s review the factors and their corresponding costs in the table below:

| Factor | Details |

|---|---|

| App Complexity |

|

| Design & UI/UX | $5K–$15K |

| Third-Party Integrations | $10K–$30K+ |

| Security & Compliance | $10K–$20K |

| Backend Infrastructure | $15K–$40K |

| Team Location |

|

| Total Estimated Cost | $50,000 to $200,000+ |

Launching a neobank app comes with its own set of challenges, many of which are unique to the banking industry. The main hurdles include:

There is immense room for improvement in neobank development, but only if you obtain licenses. This varies across different countries and is both time-consuming and expensive.

Even if you partner with a bank, there are possibilities of encountering different challenges in negotiating terms and preparing the necessary documents.

As a neobank is a part of the finance industry, fraudsters and hackers are more prone to target sensitive information. You can significantly reduce these risks by implementing robust user identification and encrypting all customer data as it is transmitted.

As a new entity, Neobanks face the challenge of convincing customers to trust them with their money, requiring strong branding, transparency, and reliable service.

A Neobank app needs to integrate seamlessly with various third-party services, such as core banking platforms, payment gateways, and credit bureaus, which can be technically complex and prone to compatibility issues.

The app’s infrastructure must be built to handle rapid user growth and increasing transaction volumes without performance degradation, requiring careful architectural planning.

Neobank app development presents a significant challenge. It must fully meet users’ evolving needs and market trends to attract attention. It is challenging to ensure a seamless user experience through personalization and gamification, while also building a secure and compliant platform.

It is recommended to create an intuitive UX with seamless onboarding, implement robust security measures, and adhere to a complex regulatory framework.

If you are looking to overcome this challenge, you can consider partnering with Moon Technolabs. We not only possess expertise in user-centric design, but we also follow advanced security protocols. Additionally, our scalable architecture and compliance-first approach will undoubtedly be helpful in developing a flawless neobank app.

Neobank development is a lucrative and promising venture for businesses looking to innovate in the financial sector. The process involves a strategic approach, beginning with thorough market research and navigating the necessary legal and regulatory requirements. From there, you’ll need a solid business plan and a team of trusted professionals to bring your vision to life.

If you’re ready to get started, the Moon Technolabs team offers a range of FinTech solutions, including neobank development. Our expertise can help you successfully launch your project. Contact us today.

01

02

03

04

Jayanti Katariya is the CEO of Moon Technolabs, a fast-growing IT solutions provider, with 18+ years of experience in the industry. Passionate about developing creative apps from a young age, he pursued an engineering degree to further this interest. Under his leadership, Moon Technolabs has helped numerous brands establish their online presence and he has also launched an invoicing software that assists businesses to streamline their financial operations.

Submitting the form below will ensure a prompt response from us.

We refine our expertise to deliver innovative business solutions.

500 N Michigan Avenue, #600, Chicago IL 60611

13500 Long Is Dr, Pflugerville, TX 78660, USA

C-105, Ganesh Meridian, S.G. Highway, Ahmedabad, GJ 380060

“ I highly recommend Moon Technolabs as the quality of service is wonderful. We have hired this company to develop the product based on some complex & technical issues. We get the best quality services as compared with others in the market. Huge Thanks to Moon Technolabs as the team is always ready to give the solution all time.”

“ Moon Technolabs is a pioneer in the WebRTC based project as they have fixed complicated segments of the module by fulfilling different product lines by providing 24X7 customer support. We really recommended Moon Technolabs as they are able to develop products as per the module deadline and project timeline.”

“I am happy to recommend Moon Technolabs for their app development services. They successfully developed apps for me, and I am highly satisfied with the overall outcomes. The development team has swiftly addressed the issues with responsive and effective communication to understand the requirement quickly and actively resolve the back-and-forth problems that arose...”

“Moon Technolabs is the best company that provides advanced apps and websites development services in the USA and Europe. I am a newbie to develop my app with an external team. I am really happy to work with them as I am not that much mobile apps user. Here, the team and specially the CEO of Moon Technolabs helps me to let me know about the benefits of my app to generate revenue....”