Table of Content

Blog Summary:

This blog provides a brief overview of the InsurTech ecosystem. This industry presents vast opportunities for innovation to both seasoned insurance companies and agile startups. Keep reading to discover more about it.

Table of Content

There has been a significant transformation in the insurance industry lately. All this is due to the recent boom in the emerging tech stacks and modern approaches to forming collaborations. This blog covers the expanding “InsurTech ecosystem”.

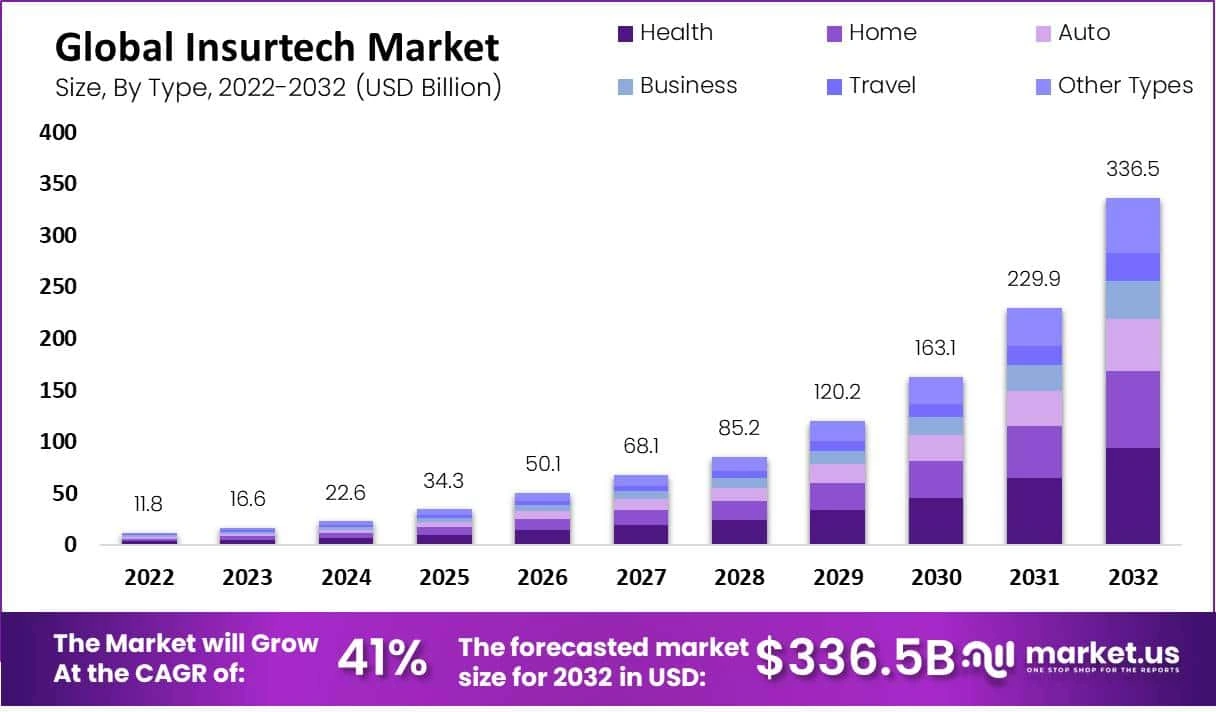

It discerns different factors stimulating invention. The InsurTech market is expected to gain significant momentum by 2028, reaching approximately USD 85.2 billion from USD 16.6 billion in 2023.

To gain a thorough understanding of the topic and develop an insurance app freely, we have created this useful guide. It will help product strategists, businessmen, and startup insurance companies.

An InsurTech ecosystem is a dynamic network of interconnected companies and stakeholders that collaborate to transform the traditional insurance industry, bringing valuable offerings to policyholders, who are the ultimate end customers.

The initiative encompasses incumbent insurers, innovative technology providers, venture capital firms, and regulatory bodies. The primary objective is to enhance efficiency, reduce costs, personalize services, and enhance the customer experience across all aspects of insurance.

This includes underwriting and claims processing, as well as risk management and distribution. Moreover, the collaborative ecosystem fosters the development of new products, services, and business models. This ultimately leads to a more seamless, data-driven, and customer-centric approach to insurance.

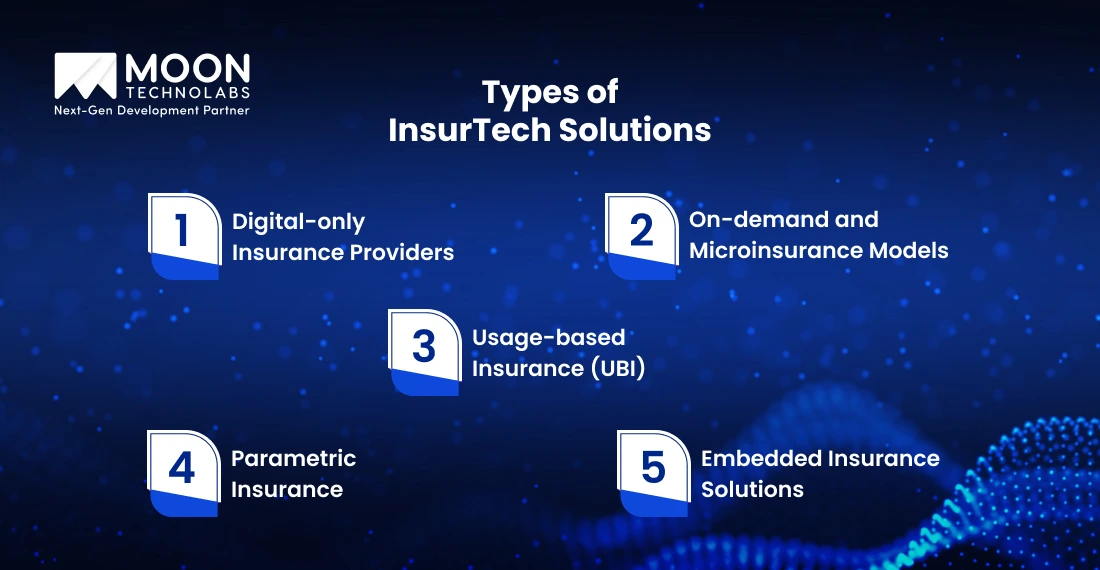

There are various InsurTech solutions designed to improve efficiency, enhance customer experience, personalize services, and reduce costs:

These are the new insurance companies that are established from scratch using digital platforms. These types of providers don’t have traditional brick-and-mortar offices. They provide a streamlined online experience for policy purchase, claims, and management. Moreover, these companies utilize data analytics and AI for underwriting and customer service.

Examples: Lemonade, Next Insurance, Hippo.

Key Characteristics: Digital customer journey, niche-oriented, lean operations, data-driven underwriting.

UBI models are also known as “pay-as-you-go” or “pay-how-you-drive” insurance. These types of solutions utilize telematics devices, which are hardware installed in vehicles or smartphone apps, to collect data on an individual’s behavior, such as driving habits and mileage. Based on the collected data, premiums are adjusted.

Examples: Snapshot by Progressive, DriveWise by Allstate.

Key Characteristics: Personalized pricing, real-time data collection, safer behavior, and dynamic premiums.

On-demand Insurance provides coverage for specific, short periods. These are particularly for events or assets and can often be activated & deactivated via a mobile app. It’s flexible and caters to temporary needs.

Microinsurance offers low-cost insurance products with small premiums and limited coverage amounts. This model is designed to protect low-income individuals and underserved populations against risks such as crop failure, illness, and other similar events.

Examples: Trov, BIMA.

Key Characteristics: Flexibility, accessibility, tailored to specific needs/risks, mobile-first.

Unlike traditional indemnity insurance that pays out based on actual losses, parametric insurance pays out a pre-agreed amount when a specific, measurable parameter or trigger event occurs, regardless of the actual damage. This could be, for example, a certain wind speed during a hurricane, a specific amount of rainfall, or a defined earthquake magnitude.

Examples: FloodFlash.

Key Characteristics: Fast payouts, transparent triggers, specific event coverage, reduced moral hazard.

Insurance coverage that is seamlessly integrated into the purchase of a product or service at the point of sale. Often, customers are unaware that they are purchasing insurance separately. It is taken as part of the overall transaction. This makes insurance easily accessible.

Examples: Device protection, travel insurance, ticket insurance for live events, and more.

Key Characteristics: Frictionless customer experience, increased conversion rates, integrated into existing customer journeys, B2B2C model.

In this model, a group of individuals pools their premiums together to cover each other’s risks. If a member makes a claim, it’s paid out from the pool. If funds remain at the end of a period, they may be returned to the members or rolled over. This model often emphasizes community and trust, and aims to reduce fraud and administrative costs.

Examples: Lemonade, Friendsurance.

Key Characteristics: Community-driven, potential for rebates, fosters trust, reduced adversarial claims process.

The InsurTech ecosystem comprises essential components, which are outlined below. Let’s check them out:

These are the new companies utilizing innovative technology to disrupt traditional insurance models. These companies focus on niche markets to introduce new products and enhance customer experiences.

These are primarily established insurance companies that are investing in and adopting emerging technologies to enhance operational efficiency. This way, they also enhance customer interactions to compete with other InsurTech companies.

Foundational technologies that power InsurTech innovations:

Government agencies and regulations that oversee the insurance industry ensure consumer protection, financial stability, and fair practices, while adapting to new InsurTech models.

Venture Capital firms and other investors provide capital to InsurTech startups, fueling their growth and innovation.

The ultimate beneficiaries of the InsurTech ecosystem are individuals and businesses seeking insurance products and services. They benefit from improved accessibility, personalized offerings, and more efficient services.

Get in touch with our expert team, who ensures the soft launch of your product within the given timeline and on budget.

InsurTech is fundamentally dependent on technology. Hence, there is a huge transformation of traditional insurance models into more efficient and personalized services. Let’s examine the technologies that are fueling this radical change:

AI and ML are substantial technologies in InsurTech. These tech stacks enable automated underwriting, personalized pricing, fraud detection, and enhanced customer service through the use of chatbots and virtual assistants.

They analyze vast data sources to identify patterns and make more accurate predictions. It also streamlines operations and helps with risk assessment.

InsurTech leverages big data from various sources, including social media, IoT devices, and public records. It then applies predictive analytics to gain deeper insights into customer behavior and risk profiles.

Consequently, this enables the development of hyper-personalized products, proactive risk mitigation, and more precise pricing, shifting away from “one-size-fits-all” policies.

IoT devices, such as wearables, smart home sensors, and connected cars, collect real-time data on policyholders’ behavior and assets. This data enables usage-based insurance (UBI), proactive risk prevention, and more accurate claims assessment. Hence, this fosters a “prevent and protect” model rather than just “pay and repair.”

Blockchain technology provides a secure, immutable, and transparent ledger for recording transactions and policy details. In claims processing, it automates payouts through smart contracts, reduces fraud, and increases trust among all parties by providing a persistent record of events. This speeds up resolution times and enhances transparency among companies.

Cloud computing provides scalable, flexible, and cost-effective infrastructure for InsurTech companies. This way, they can quickly develop, deploy, and scale new applications and services without significant upfront investments in hardware.

This ultimately facilitates rapid innovation, accelerates time-to-market for new products, and seamless integration with other technologies and partners.

The InsurTech ecosystem offers several major benefits, which are as follows:

Insurtech companies are utilizing innovative technologies to transform and disrupt the traditional insurance industry, providing more personalized, efficient, and accessible services. Here are some real-world examples:

Lemonade uses artificial intelligence (AI) and machine learning to automate the claims process. The company’s chatbot, “AI Jim,” is capable of reviewing claims, cross-referencing policies, running anti-fraud algorithms, and even approving and processing payments in seconds.

This drastically reduces claim processing times and improves customer satisfaction.

Root Insurance utilizes telematics technology (via a mobile app) to track real-time driving behavior (speed, braking, etc.). This allows them to offer highly personalized insurance rates based on actual driving habits rather than traditional demographic factors. Good drivers receive lower premiums, making insurance fairer and often more affordable.

Trōv pioneered “on-demand” or “micro-insurance,” allowing users to insure specific items (such as a camera or a bicycle) for a specific period, entirely through their smartphone. This offers unprecedented flexibility and control, appealing to younger, digitally-native generations who prefer to insure only what they need, when they need it.

(Note: Trōv has since shifted to a B2B model, providing its technology to other insurers for embedded insurance solutions).

BIMA focuses on providing affordable, accessible insurance and health services to low-income populations in emerging markets, primarily through mobile technology.

They leverage mobile networks to register customers, collect premiums, and facilitate claims, reaching millions who previously had no access to formal financial protection, often for risks like the death or illness of a breadwinner.

Metromile (now part of Lemonade) offers a unique “pay-per-mile” auto insurance model. By installing a small device in the car’s diagnostic port and using a smartphone app, they track the miles driven.

Customers pay a low base rate plus a per-mile fee, which significantly benefits low-mileage drivers, urban residents, and remote workers who might otherwise overpay for traditional flat-rate policies.

However, there are many hurdles in the InsurTech ecosystem. It faces several significant challenges, including:

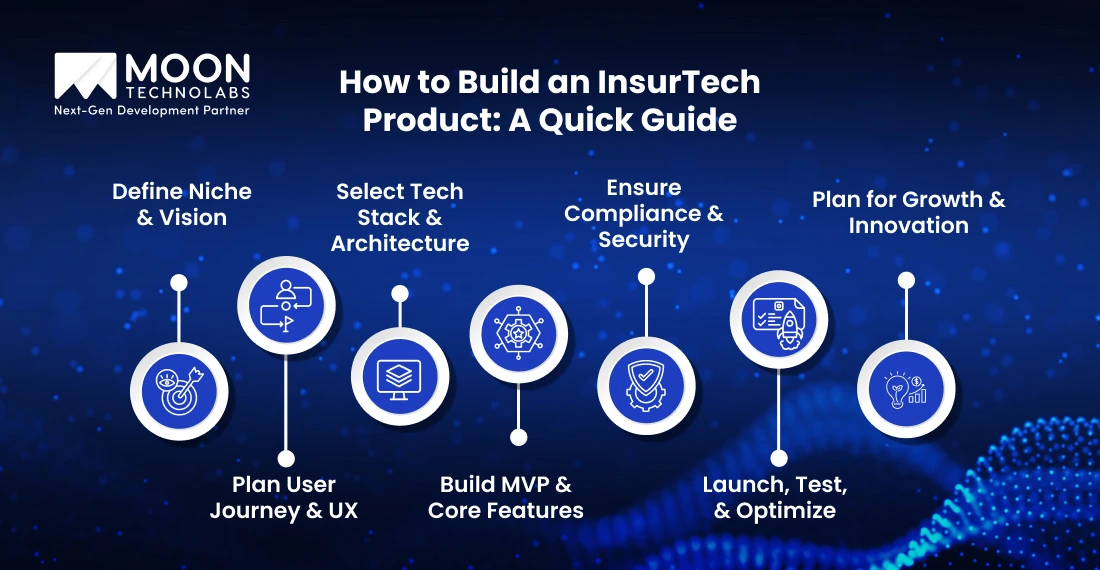

InsurTech product development involves a systematic approach, starting with thorough market research to identify unmet customer needs and a clear value proposition. The process includes agile development, rigorous testing, and continuous iteration to ensure a robust, compliant, and market-ready product.

Let’s analyze the process step-by-step:

This crucial initial phase involves conducting in-depth market research to identify underserved segments within the insurance industry. Are you targeting small businesses, specific high-risk professions, or a niche market, such as pet insurance with a modern twist?

Once you pinpoint your target audience, you need to clearly articulate the problem your product solves and how it will disrupt or improve existing insurance processes. Your product vision should outline the core value proposition and what makes your offering unique and compelling.

InsurTech products thrive on user-friendliness. This step focuses on creating a seamless and intuitive experience for your customers. Map out every interaction a user will have with your product, from initial discovery and quote generation to policy management and claims processing.

Develop wireframes and prototypes to visualize the flow, ensuring clarity, simplicity, and efficiency. A strong UX strategy minimizes friction, builds trust, and encourages adoption.

The technological backbone of your InsurTech product is vital for performance, scalability, and security. This involves selecting programming languages, frameworks, databases, and cloud infrastructure that align with your product’s requirements.

Consider factors like real-time data processing, API integrations with existing insurance systems, and the need for advanced analytics or AI capabilities. A well-designed architecture ensures your product can handle increasing user loads and evolving features.

An MVP (Minimum Viable Product) is a version of your product with just enough features to satisfy early customers and provide valuable feedback for future product development. Focus on implementing the absolute core functionalities that deliver your primary value proposition.

This might include a streamlined quoting engine, basic policy issuance, or a simple claims submission portal. Integrate essential APIs (e.g., for payment gateways, identity verification, or external data sources) to make the MVP functional.

The insurance industry is heavily regulated, making compliance a non-negotiable aspect of InsurTech development. This step involves understanding and adhering to relevant insurance laws, data privacy regulations (such as GDPR or local equivalents), and cybersecurity standards.

Implementing robust security measures is crucial for protecting sensitive customer data, preventing fraud, and maintaining trust. Legal counsel and compliance experts are essential at this stage.

Once your MVP is ready and compliant, it’s time for a controlled launch. This could involve a pilot program with a small group of users or a soft launch to gather initial feedback. Rigorous testing, including unit testing, integration testing, and user acceptance testing (UAT), is crucial for identifying and resolving bugs.

Post-launch, continuously monitor user behavior, gather feedback, and use data analytics to identify areas for improvement. This iterative process of optimization ensures your product evolves based on real-world usage.

A successful InsurTech product must scale to accommodate a growing user base and increasing transaction volumes. Plan for infrastructure upgrades, database optimizations, and a flexible architecture that can support new features and integrations.

Apart from scaling, continuous innovation is key to staying competitive. This involves regularly exploring new technologies (such as AI and blockchain), market trends, and customer needs to enhance your product and maintain its relevance in the rapidly evolving InsurTech landscape.

The future outlook of the InsurTech domain is quite bright in many aspects. It has immense possibilities for insurance businesses. Let’s check it out.

Generative AI in Customer Service will revolutionize how insurers interact with customers. Be it automating responses, personalizing communication, or streamlining processes such as claims management and policy inquiries. Hence, it will lead to faster, more efficient, and satisfying customer experiences.

Insurers are leveraging AI, data analytics, and real-time data from sources like wearables and telematics to create highly customized policies and pricing. This moves away from “one-size-fits-all” to offer coverage tailored to individual behaviors, needs, and risk profiles.

Collaboration between InsurTech and other sectors, particularly Healthtech, is growing. This enables innovative solutions that integrate insurance with broader health management, leveraging data and technology to create more comprehensive offerings and proactive risk management strategies.

Insurance is increasingly being integrated seamlessly into the purchase of other goods and services, often at the point of sale on digital platforms. This “embedded” approach makes insurance more convenient, accessible, and relevant, often leading to the development of micro-insurance models.

InsurTech is rapidly expanding into developing economies, particularly in Asia, Latin America, and Africa. These markets, characterized by large underinsured populations and increasing digital adoption, represent significant growth opportunities for companies offering affordable, mobile-first, and customized insurance solutions.

From automation to customer experience, our InsurTech solutions are built to transform your workflow. Our experts are here to guide you through innovative tools tailored for your business.

The InsurTech landscape is ripe with immense opportunities, but to truly capitalize on it, you need to bring impactful insurance app ideas to life. If you’re looking to launch a high-performing digital insurance product, Moon Technolab’s technical experts can transform your vision into a market-ready solution.

Our commitment to excellence in insurance software development is clear. Our dedicated engineers and designers specialize in crafting successful insurance solutions that stand out. If you’d like to explore how we help your product stand out in the InsurTech space, contact us today.

01

02

03

Jayanti Katariya is the CEO of Moon Technolabs, a fast-growing IT solutions provider, with 18+ years of experience in the industry. Passionate about developing creative apps from a young age, he pursued an engineering degree to further this interest. Under his leadership, Moon Technolabs has helped numerous brands establish their online presence and he has also launched an invoicing software that assists businesses to streamline their financial operations.

Submitting the form below will ensure a prompt response from us.

We refine our expertise to deliver innovative business solutions.

500 N Michigan Avenue, #600, Chicago IL 60611

13500 Long Is Dr, Pflugerville, TX 78660, USA

C-105, Ganesh Meridian, S.G. Highway, Ahmedabad, GJ 380060

Ayse D.

Co-Founder“ I highly recommend Moon Technolabs as the quality of service is wonderful. We have hired this company to develop the product based on some complex & technical issues. We get the best quality services as compared with others in the market. Huge Thanks to Moon Technolabs as the team is always ready to give the solution all time.”

Justin G.

Founder & CEO“ Moon Technolabs is a pioneer in the WebRTC based project as they have fixed complicated segments of the module by fulfilling different product lines by providing 24X7 customer support. We really recommended Moon Technolabs as they are able to develop products as per the module deadline and project timeline.”

Flavio S.

Founder & Managing Director“I am happy to recommend Moon Technolabs for their app development services. They successfully developed apps for me, and I am highly satisfied with the overall outcomes. The development team has swiftly addressed the issues with responsive and effective communication to understand the requirement quickly and actively resolve the back-and-forth problems that arose...”

Jay M.

Founder & CEO“Moon Technolabs is the best company that provides advanced apps and websites development services in the USA and Europe. I am a newbie to develop my app with an external team. I am really happy to work with them as I am not that much mobile apps user. Here, the team and specially the CEO of Moon Technolabs helps me to let me know about the benefits of my app to generate revenue....”

Our Offices

India

C-105, Ganesh Meridian, S.G. Highway, Ahmedabad, GJ 380060USA

500 N Michigan Avenue, #600, Chicago IL 60611Contact Information